Another week of the COVID-19 pandemic crisis has passed, and OrthoFi is upholding its commitment to keep the industry informed. As weeks without new start production stack up, the impulse to panic potentially becomes stronger. This is why it is important for you to be grounded in facts, and to be as data-driven as possible. We have data on over $2.2 Billion of production we’ve processed in over 385 orthodontic practices (500+ locations), and outcomes on over $500 Million in active patient and insurance A/R. As part of our pledge, OrthoFi will continue to share weekly data on the key metrics that matter.

The data in the charts presented below is aggregated by week, with the date being the start of the week. The latest data set is the week of April 12th to 18th. Our next update will include data from April 19th through April 25th.

Exams by Type – Are Practices Focusing On the Right Areas?

Our CRM software platform tracks exams by date, time, and type. Exam types include: New Patient Exam (NPE); Observation (Obs); Recall Ready (designated by the practice); and Phase 2. Below is the latest breakdown of scheduled exams by type and by the week they were scheduled:

As you can see, the vast majority of scheduling activity is around New Patient Exams (NPEs). A much smaller portion of scheduled exams are Observation and Recall Ready, with almost no Phase 2 exams. In this unique time, given health and safety concerns, it is a common assumption that consumer demand is suppressed. While virtual consults are incrementally opening opportunity for new patient production, this is not the lowest hanging fruit. During times of low demand, the best strategy is often mining your “piggy bank” opportunities.

Your Obs and Phase I patients represent a fertile group to mine from and are far more likely to yield successful virtual consult conversions, which can be stacked up and scheduled as soon as your office is ready to reopen. These are patients who already know you and your team, have already experienced the splendor and technology of your office, and thus have fewer apprehensions about starting treatment with you. New patients may want treatment for themselves or their children, but they are not as connected to you, and although a well-done virtual consult allows them to meet you and see the value of starting with you, they can also shop around with less effort during this time. We suggest taking time to mine your reports and schedule patients in the following populations (in priority order):

- Patients you have designated as recall ready (i.e. ready to start treatment) before the crisis

- Observation patients by age and date of last visit

- Pending patients, with an extra focus on exams within the 4-6 weeks prior to the COVID closures

- Phase I patients who are between phases and could likely be ready for Phase II

Practice Closures and Exam Dates – UPDATE

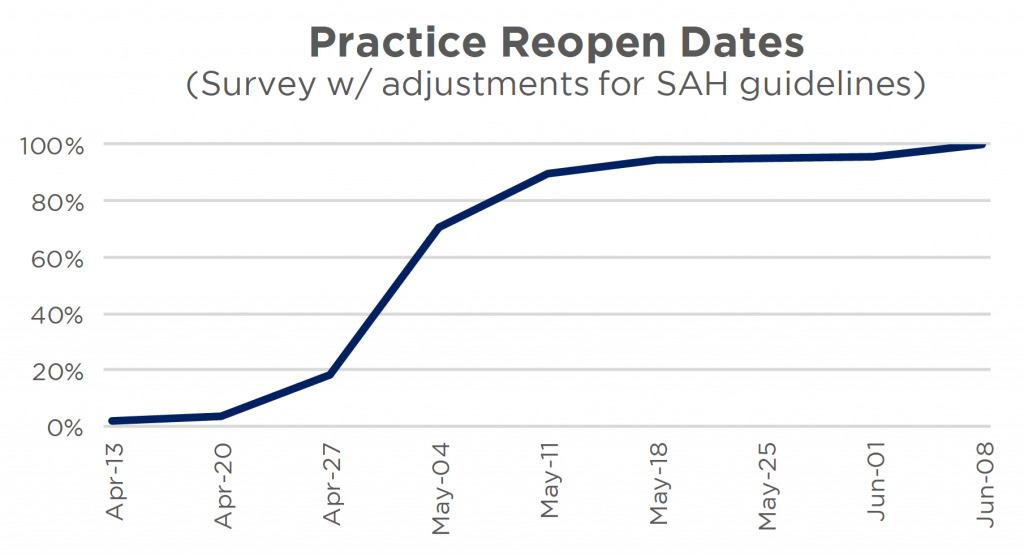

Delivering industry-leading Revenue Cycle Management (RCM) services requires accurate new case volume forecasting to scale staffing. To do this, OrthoFi compares scheduled exam data with practice survey data. We continue to survey our 385 practices weekly, asking them when they predict to reopen. The graph below shows the latest collective response to those surveys:

The responses reflect the latest published updates in state-mandated guidelines. As shown, 70% of practices are anticipating to reopen the week of May 4th and over 80% the week of May 11th, which parallels the guidelines in most states, with some East and West coast states moving to adopt more conservative measures.

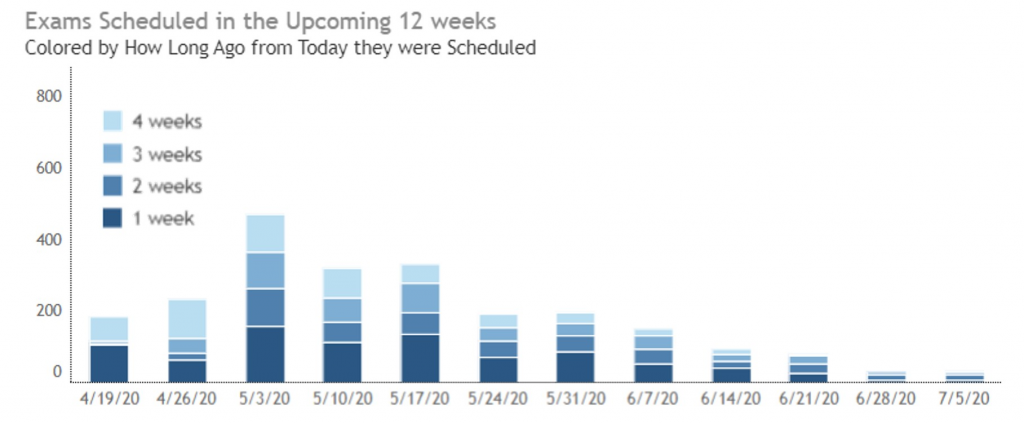

How does this information compare with our data on scheduled exams? The chart below shows exams scheduled by week, and within that, how many weeks ago those exams were actually scheduled. This provides a glimpse into the most recent trend in scheduling activity across the country. We use this data to scale the staffing of our OrthoFi service teams.

As indicated by the survey, there is a notable increase in exams created for the week of May 3rd, but the total volume of exams does not match up with the responses in the survey above. Typically, our practices see between 7,000-8,000 exams per week. If 80% of practices were to open, we would expect to see over 5,000 exams scheduled for that week. We assume this discrepancy relates to practices taking a cautious approach to scheduling in response to how often reopen dates have pushed out over the last 6 weeks. Until practices are certain that they will be able to open, they may be hesitant to set their schedules.

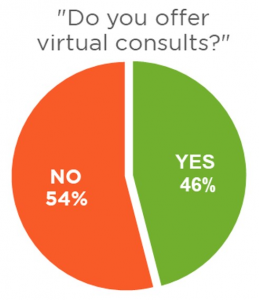

Last week we published the responses from our first survey of practices offering virtual consults (VCs). At that time, 38% of practices indicated they were offering this service to new and existing patients. In just one week that number has now jumped to 48%. This is an indication that web learning on this technology has been impactful. With a fully digital workstream, innovative practices are finding they can not only consult with patients remotely, but can also convert a fair number of these patients into starts, obtaining signed contracts and down payments. For more information on how to incorporate virtual consults into your processes, watch our latest webinar and our recent Same-Day Starts MasterClass featuring Dr. Jamie Reynolds, Danielle Offerman, Dr. Alexander Waldman, and Brian Wright.

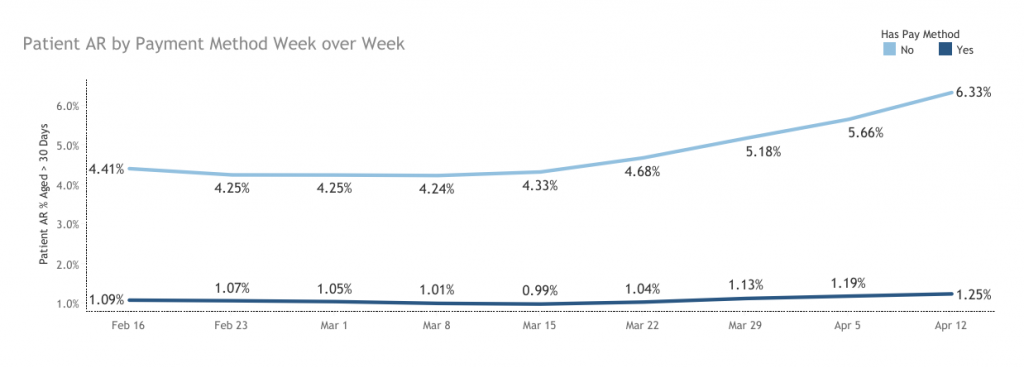

Patient A/R – UPDATE

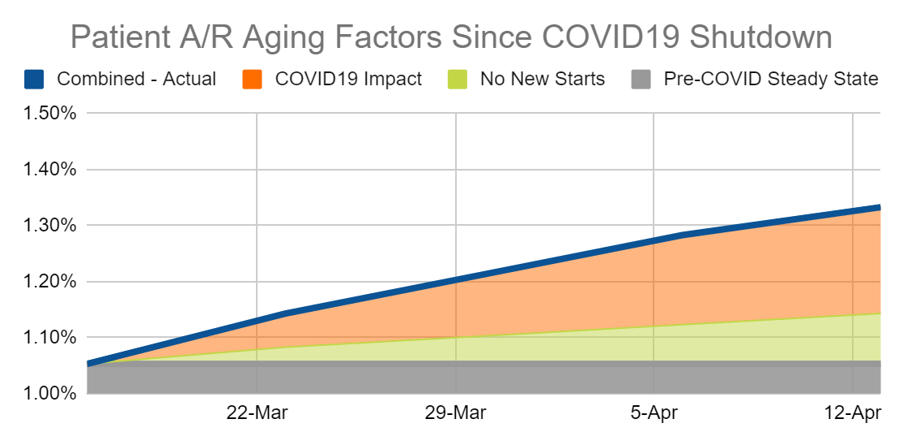

With the global pandemic’s impact on the economy, practice owners are concerned about their collections and increasing delinquency during the shutdown. As reported in the previous two articles, our autopay payment success rate has not changed since the onset of this crisis. We are seeing the same percentage of credit cards and ACH withdrawals go through successfully. However, we are seeing an overall increase in our A/R aging >30 days. As discussed in our most recent update, there are two driving factors for this: no new starts, and patient payment behavior due to economic pressures. For a more detailed explanation of how to interpret the segments in the chart below, read last week’s article.

This week’s update shows a continued increase in overall A/R aging, with the ratio of factors staying fairly consistent. No new starts still represents roughly 1/3 of the change, with change in patient payment performance being the remaining 2/3. When practices reopen, we project that the infusion of A/R from new starts production will quickly slim down the green section. However, it will take some time to reduce past due balances from patients who have been impacted financially.

How can you minimize delinquency and avoid default in the long term? Aside from maintaining tight disciplined collection protocols, the clearest area of focus from the data is autopayment implementation. The chart below is an update of last week’s article, showing the overall week-over-week patient A/R performance filtered by accounts with autopay vs. those with no autopay payment method on file.

As we’ve been reporting, we continue to see an increasingly widening separation of A/R performance between accounts with and without autopay. We project this trend to continue to accelerate. Although those with autopay do show an expected rise in past due aging pre- and post-COVID (roughly 10% once you factor out the effect of no new starts), the accounts without autopay on file reveal a very different picture.

Since February 16th, non-autopay accounts have seen a 44% increase in delinquency, and almost 66 basis points higher in just the last week. Thankfully, this population only accounts for a small portion (9%) of OrthoFi’s overall accounts receivable, so our overall A/R aging trend is flatter than what individual practices may see. In your practice, if you have not implemented autopay or have not been diligent about requiring it when patients sign their contracts, your patient A/R might be at greater risk. Read our first article for more insights and guidance on this topic.

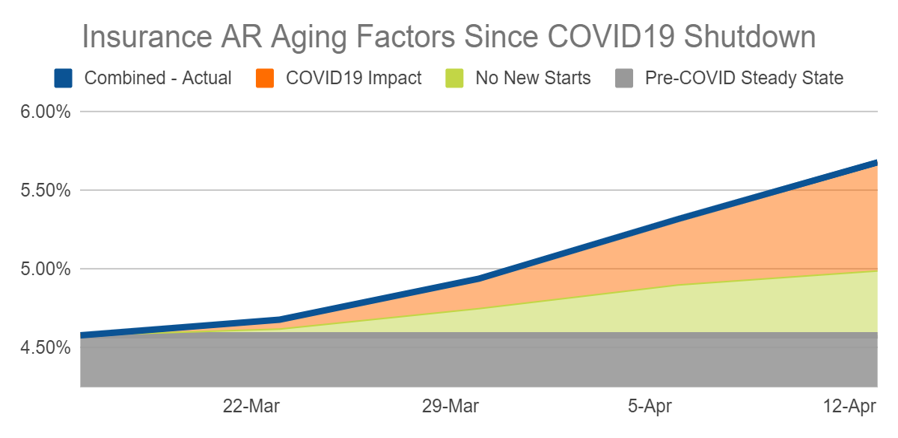

Insurance A/R – UPDATE

As reviewed in our most recent update, there are two driving factors for this: no new starts, and insurance carrier remittance delays due to carrier closures and broader trends of leaner staffing. For a more detailed explanation of how to interpret the segments in the chart below, read last week’s article.

This week’s update shows that the impact of no new starts is linear and consistent. It is increasing proportionally with time. The impact of COVID-19 seems to be increasing at a faster rate, representing 63% of the increase in claim aging this past week vs. 56% the previous week. We have not yet seen a spike in plan terminations due to unemployment, but this may be an early indicator that these are coming. Aside from that, unlike the COVID-19 impact on patient A/R, there is no real risk that insurance carriers won’t be able to pay. Once practices reopen and start seeing new start production, we project this swell of past-due claims to recede, as well as the effect from no new starts.

***Benefit Termination Alert: OrthoFi is closely monitoring the impact of unemployment on insurance receivables. Families who lost their benefits due to a layoff (vs. retaining them with a time-based furlough) will face termination of coverage. For terminated plans, insurance balances will need to be transferred to the patient responsibility, at least in the short term, until there is confirmation of new, valid coverage. Practices managing their A/R in-house will need to coordinate this shift. This will be more challenging for accounts already in delinquent status, therefore, be sure to work diligently to keep accounts in good standing throughout this time. As we start to see actionable data and outcomes, we will add this to our updates going forward.

Takeaways – What The Data Tells Us

Several of these takeaways are repeated from previous weeks, but they continue to be critical.

- As you prepare or plan to reopen, be strategic with your opportunities. Simply offering ways for new patients to reach you will likely yield less return than focusing on the stored opportunities within your management system.

- Practices around the country are tentatively planning to reopen in early May, but the uncertainty of stay-at-home guidelines are causing hesitation to schedule exams.

- The number of practices offering virtual consults is rising quickly with some early success.

- Patient A/R delinquency has not increased exponentially within our patient pool, but there has been some impact due to not having starts and macroeconomic effects on patient payment performance.

- Monitoring your patient A/R regularly and being prompt with your delinquent follow-ups is more important than ever – especially with those accounts who do not have autopay.

- Insurance is paying slower and requiring more follow-up to secure consistent collections. Ensure you have someone consistently monitoring your insurance A/R to keep things on track.

- Unemployment Foreshadowing: As layoffs lead to insurance coverage termination, more pressure will shift to patient collections. Financial coordinators need to remain diligent in their efforts to keep accounts in good standing and to avoid a mass amount of unplanned insurance balances with past-due patient responsibility.

We hope this data can be a valuable resource during this time. We will continue to update these metrics, and add new areas of focus as new meaningful trends emerge.

If you want to automatically receive these updates, please follow us on Facebook. If you have any questions you’d like us to answer, please post your question on our page, or visit us at StartMoreSmiles.com to connect with one of our practice experts.