It looks as if there may be a light at the end of this very dark tunnel. A high number of states have either opened restrictions or are making concrete plans to stage a reopening. The climb back for our industry will be interesting, and OrthoFi is committed to report on how this progresses. We have data on over $2.2 Billion of production we’ve processed in over 385 orthodontic practices (500+ locations), and outcomes on over $500 Million in active patient and insurance A/R. As part of our pledge, OrthoFi will continue to share weekly data on the key metrics that matter.

The data in the charts presented below is aggregated by week, with the date being the start of the week. The latest data set is the week of April 26th to May 1st. Our next update will include data from May 3rd to the 9th.

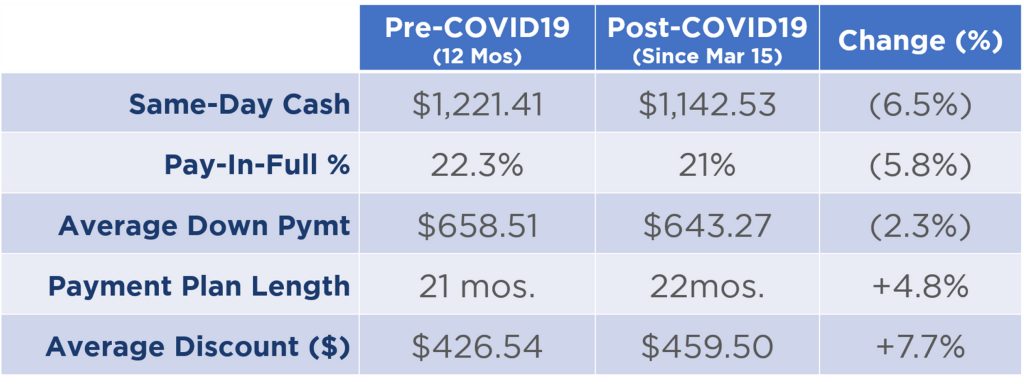

Payment Terms – How Has the Crisis Impacted Terms and Affordability?

As we approach the imminent reopening of practices and patients come back in to seek treatment, many practice owners are concerned about how to position their fees in the face of an unprecedented economic shutdown. It’s hard to ignore the headlines detailing depression-level unemployment and small business interruption. There is fear that patients will not be able to afford treatment, or will shop more aggressively on price to get lower fees. During our Same-Day Start Master Class Online Course last week, we fielded several questions about how to address these hardships. In anticipation of that concern, we have pulled a report to show the change in payment terms since the crisis began. The chart below shows the terms on contracts signed since March 15th, primarily outcomes of virtual consults without fixed start dates.

What we see is that there has been very little impact to overall payment terms and patient affordability. If the average family were heavily impacted and experiencing undue cash flow tightness, you’d expect to see a sharp drop in Pay-In-Full (PIF) frequency, as well as average down payments. However, you can clearly see that PIFs are fairly stable, dropping just 5.8%. Average down payments are down a relatively insignificant 2.3%.

At OrthoFi, we measure and report on what we call Same-Day-Cash (SDC), which is the blended average of all PIFs and down payments. The combined same-day-cash is down only 6.5%, and payment plan length has only extended by one month, both remarkably small changes given the current circumstances. Note: this data is captured from patient selection within an open-choice payment slider model (either via in-consult presentation or through our NEW Sign@Home feature), where our practices’ patients are encouraged to choose their own payment options, in which they are most often given the flexibility to put down as little as $250 and pay for as long as 36 months.

Given the choice, patients are choosing options nearly identical to those prior to the crisis. The changes do show that some patients have been acutely affected, but indications are that the swift stimulus measures to supplement furloughed or reduced wages have created a measure of income and consumer behavior stability. A small minority of plans is moving the fleet average, but not very much.

So what does that mean for you?

It means that you shouldn’t assume patients’ finances demand lower down and monthly terms, but you should be prepared if they do. The key is to offer open choice, a way to address acute needs when they present themselves, without affecting your default term offers which will certainly impact your cash flow. Some OrthoFi practices have been a bit more aggressive with courtesy discounts, mostly to create greater urgency to sign during practice closure and to reward higher down payments to manufacture cash flow. This increase is also relatively contained, indicating that they have not felt the need to drop fees dramatically to get patients to sign.

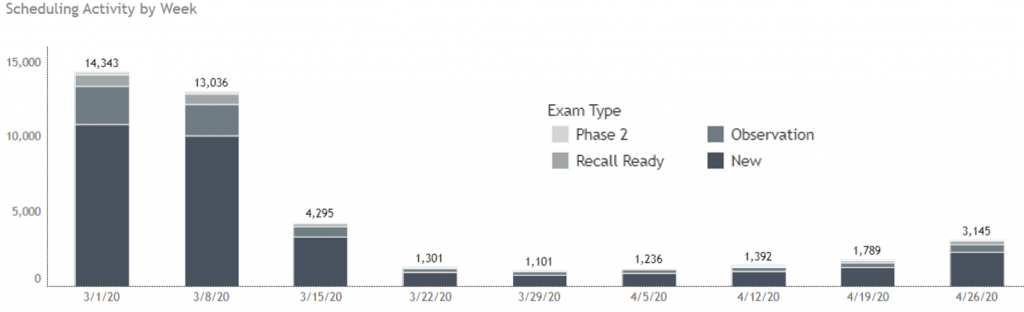

Exams – Proof of Life

Our CRM software platform captures exam dates, and when they were scheduled. As expected, the closure and uncertainty about reopening dates has cratered exams and scheduling activity. Below is a chart which shows overall exam scheduling activity by week.

As you can see, scheduling activity fell sharply the week the first stay-at-home guidelines were released. Since then, scheduling volume has been consistently low, hovering around 10% of pre-COVID levels. As news of states lifting restrictions started filtering in at the end of last week, you can see the increase of recently scheduled exams. Last week’s activity was nearly double that of the week prior. We anticipate this coming week will see a sharp increase in scheduling. Exam type is still heavily weighted to new patient exams. Read our last article to see insights on potentially more lucrative exam prioritization strategies.

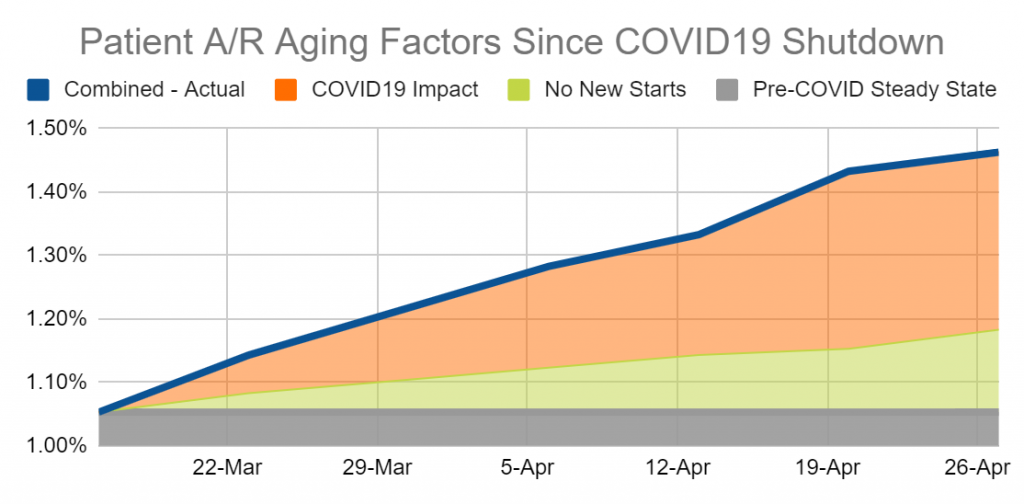

Patient A/R – UPDATE

Since many practices furloughed entire teams and essentially froze financial coordinator activity, practice owners are concerned about their collections and increasing delinquency during the shutdown. As reported in the previous articles, our autopay payment success rate has not changed since the onset of this crisis. We are seeing the same percentage of credit cards and ACH withdrawals go through successfully. However, we are seeing an overall increase in our A/R aging >30 days. As discussed in our second update, there are two driving factors for this: no new starts, and patient payment behavior due to economic pressures. For a more detailed explanation of how to interpret the segments in the chart below, read our Week 2 article.

This week’s update shows a continued increase in overall A/R aging, albeit still within an industry-acceptable range. No new starts still represents roughly ⅓ of the change, with change in patient payment performance being the remaining ⅔. The COVID19 impact has accelerated, mostly due to the continued erosion within accounts without autopay (see chart below). When practices reopen, we project that the infusion of A/R from new starts production will quickly slim down the green section. However, it will take some time to reduce the past due balances from patients who have been impacted financially.

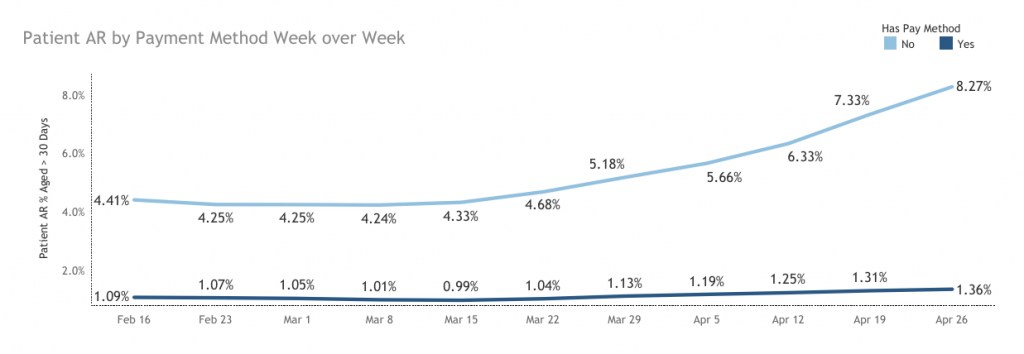

What can you do to bring your A/R aging back into control when you resume operations? Aside from maintaining tight disciplined collection protocols, the clearest area of focus from the data is autopayment implementation. The chart below is an update of last week’s article, showing the overall week-over-week patient A/R performance filtered by accounts with autopay vs. those with no autopay payment method on file.

As we’ve been reporting, we continue to see an increasingly widening separation of A/R performance between accounts with and without autopay. We project this trend to accelerate until practices come back and initiate efforts to contact and schedule past due patients. Although those with autopay do show a relatively small but expected rise in past due aging pre- and post-COVID (roughly 12% once you factor out the effect of no new starts), the accounts without autopay on file reveal a very different picture. Since February 16th, non-autopay accounts have seen an 87.5% increase in delinquency, and almost 95 basis points higher in just the last week. Thankfully, this population only accounts for a small portion (9%) of OrthoFi’s overall accounts receivable, so our overall A/R aging trend is flatter than what individual practices may see.

In your practice, if you have not implemented autopay or have not been diligent about requiring it when patients sign their contracts, your patient A/R might be at greater risk. Read our first article for more insights and guidance on this topic.

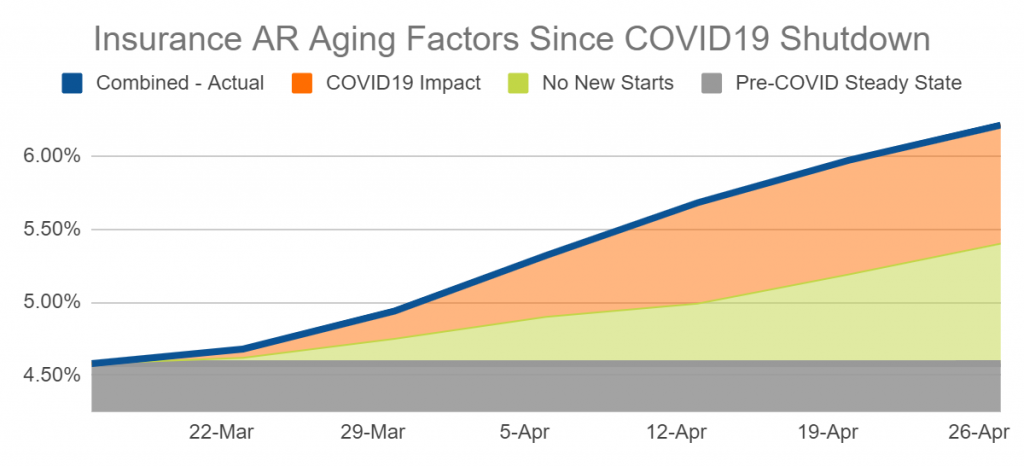

Insurance A/R – UPDATE

As reviewed in our most recent update, there are two driving factors: no new starts, and insurance carrier remittance delays due to carrier closures and broader trends of leaner staffing. For a more detailed explanation of how to interpret the segments in the chart below, read last week’s article.

This week’s update shows that the impact of no new starts is linear and consistent. It is increasing proportionally with time. We have not yet seen a spike in plan terminations due to unemployment, which we believe are coming. Aside from that, unlike the COVID-19 impact on patient A/R, there is no real risk that insurance carriers won’t be able to pay. Once practices reopen and start seeing new start production, we project this swell of past-due claims to recede, as well as the effect from no new starts.

***Benefit Termination Alert: OrthoFi is closely monitoring the impact of unemployment on insurance receivables. Families who lost their benefits due to a layoff (vs. retaining them with a time-based furlough) will face termination of coverage. For terminated plans, insurance balances will need to be transferred to the patient responsibility, at least in the short term, until there is confirmation of new, valid coverage. Practices managing their A/R in-house will need to coordinate this shift. This will be more challenging for accounts already in delinquent status, therefore, be sure to work diligently to keep accounts in good standing throughout this time. As we start to see actionable data and outcomes, we will add this to our updates going forward.

Takeaways – What The Data Tells Us

Several of these takeaways are repeated from previous weeks, but they continue to be critical.

- Patient payment plan selections have not materially changed since the crisis, so practices should leverage an open choice model to ensure they are prepared to be flexible without changing their default term options.

- Practices around the country are tentatively planning to reopen in early May, and exam scheduling is finally starting to parallel those plans, albeit still at a reduced rate.

- Monitoring your patient A/R regularly and being prompt with your delinquent follow-ups is more important than ever – especially with those accounts who do not have autopay.

- Insurance is paying slower and requiring more follow-up to secure consistent collections. Ensure you have someone consistently monitoring your insurance A/R to keep things on track.

- Unemployment Foreshadowing: As layoffs lead to insurance coverage termination, more pressure will shift to patient collections. Financial coordinators need to remain diligent in their efforts to keep accounts in good standing and to avoid a mass amount of unplanned insurance balances with past-due patient responsibility.

We hope this data can be a valuable resource during this time. We will continue to update these metrics and add new areas of focus as new meaningful trends emerge.

If you want to automatically receive these updates, please follow us on Facebook. If you have any questions you’d like us to answer, please post your question on our page, or visit us at StartMoreSmiles.com to connect with one of our practice experts.