In previous posts (found on Orthopundit.com), I shared some of the learnings we have found from aggregate data collected by OrthoFi. Time has passed since our initial posts, and we have continued to study and learn from the data collected from over 500,000 starts with over $2 billion in orthodontic production. This year, we plan to share more information with posts on the Pragmatic Orthodontist and the OrthoPreneurs online groups. Today we discuss benchmarking and evaluating credit card processing fees.

To understand what you’re paying for, the first things you need to “process” are the following terms:

Merchant: The person in the transaction that is selling goods or services. For purposes of this post, the merchant is the orthodontic office. The other parties in the purchase are the customer, the bank, and the credit card processor.

Interchange Fees: Fees that the merchant’s (ortho office) bank account must pay whenever a customer uses a credit/debit card to make a purchase. The fees are paid to the card-issuing bank to cover handling costs, fraud and bad debt costs, and the risk involved in approving the payment.

True Transaction Costs: The interchange fees plus all the additional fees associated in processing a sale. These fees can happen per transaction or as part of a monthly charge, membership fee, or similar recurring cost. As I will explain, here’s where the non-advertised costs frequently occur.

While there are other fees that merchants (orthodontists in this case) pay for the privilege of making sales via credit and debit card, interchange fees are by far the largest representing 70% to 90% of the total fees paid to banks by merchants. These interchange fees (commonly a percentage of the total sale plus an additional per transaction flat fee) change throughout the year as cost of money changes with interest rates, etc. We all know the interest rates that apply to loans (e.g. your mortgage) change frequently. The same applies to credit card interchange rates. For example, Visa and MasterCard set new interchange fees twice a year.

Any business that allows customers to make purchases with credit/debit cards has to pay interchange fees. While no retailer likes to see potential profits deducted from a sale, the net gain from accepting credit/debit cards far outweighs the cost of interchange fees. This includes accepting higher fee cards like Discover and American Express.

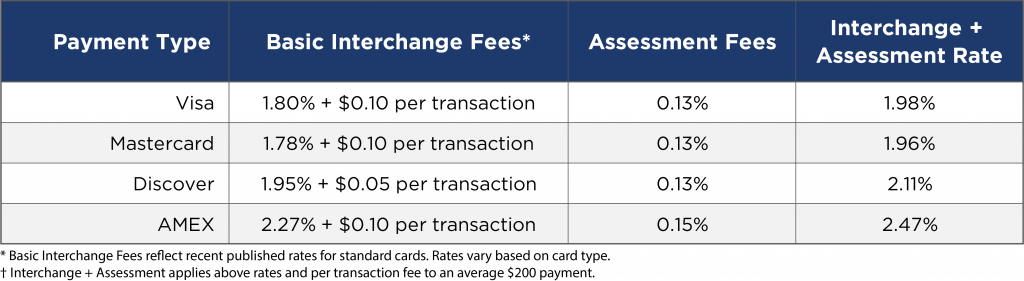

Interchange fees vary due to a variety of factors: payment type, whether the card is a secured-funds debit card vs a credit card, swiped vs the numbers manually entered in, if the card has rewards/perks tied to it, etc. All these charges impact the final transaction cost relayed to you. On top of interchange, all the major credit card networks make their money by adding assessment fees, which commonly range from 0.13% to 0.15%. The chart below lists the latest basic interchange rates:

The chart above reflects what goes to the credit card network companies (VISA, MC, Discover, AMEX). Credit card processing companies, like the ones you deal with, have to pay for operating costs and build their margin from there. Think of these companies as the middlemen that operate between the credit card companies and the orthodontist. We don’t deal directly with Visa, MasterCard, etc. The processing companies act on our behalf, adding to the total transaction costs.

When advertising the ‘rate’, processing companies typically show a blended rate (rates of all the card types averaged together) averaged again with a ‘typical usage mix’ of these cards. The actual rate will vary based on the amount of each transaction processed by each particular card type.

Most of us look at the blended interchange rate and mistakenly take that number as the true transaction cost. In fact, you may think you’re paying lower rates than what is shown above because of how the rates are marketed. Payment processors aggressively compete on published rates, some even going below interchange to win the business, knowing they will get it all back by tacking on extras.

Believe it or not, vendors can be quite deceptive about the total amount in fees you pay per transaction as they know that most people only look at the ‘rate’ and not all the other costs associated with using the service. One vendor many orthodontists use even goes so far as to send two separate statements with transaction rates on one statement and all the other fees associated with their service on a separate statement. These statements are sent separately to keep you from connecting the dots. Other times, important information about extra fees you pay are buried in the fine print of your statements or service agreements. There are a number of additional fees that can be present in the transaction cost we should know about and understand. Here are some of the common ‘hidden’ fees to consider:

Per-Transaction Fee: An additional fee that you pay per transaction on top of the negotiated interchange per transaction fees shown above. You would think the advertised rate would be what you actually pay, but many companies charge an additional rate on top of the interchange rate. As I said, many companies dangle low rates, but then make it up with additional per-transaction fees ranging from $0.25 to as high as $1.60 per payment received. That’s almost a whole percentage point if you consider that most of your transactions are between $180-200.

ACH/CC Failed Payment & Chargeback Fees: Failed payment fees are assessed if a payment fails or insufficient funds are in the account. Chargebacks happen when the consumer requests a stop payment or refund directly from their bank (rather than calling the office to request a refund). Although

they happen infrequently, these fees can range up to $25 per incident, so they often affect your overall annual cost.

PCI Compliance/Non-Compliance Fee: The Payment Card Industry Data Security Standard (PCI DSS) applies to companies of any size that accept credit card payments. If your company intends to accept card payment or to store, process and transmit cardholder data, you need to host your data securely with a PCI compliant hosting provider. Even though this is a mandatory part of processing payments, many processing companies pass this on as additional fees, ranging up to as much as $30 per month.

Membership / Maintenance Fee: Think of this like the annual fee you pay for certain credit cards. Certain processing vendors also charge an ‘annual fee’ or monthly ‘maintenance fee’. This should be added to the interchange rates they advertise as this increases the out of pocket dollars you are spending to process payments. These often range from $25 to $39 per month.

Charge per Online Payment or New Payment Method: These fees are typical with some auto-pay vendors, where you pay for the ‘setup’ of each new automatic payment in the event the patient changes their payment method. Again, these add another $0.25 to $0.50 per incident, which can add up over hundreds of open accounts over multiple years.

The presence or absence of these additional fees will impact the overall amount you pay for payment processing and, therefore, should be considered in the total cost of doing business with a particular vendor. The interchange fee alone is typically not all that you are paying for processing.

Get out your calculator: The easiest way to know your True Transaction Cost is to calculate the total difference between the total amount processed and the net amount deposited into your account after all the fees, ‘discounts’, and deductions, then divide that by the gross. Warning: the results may shock you.

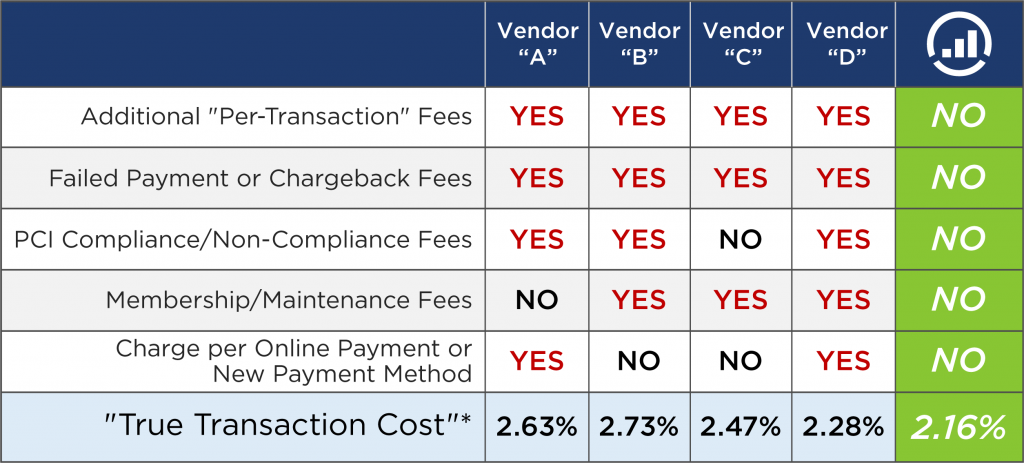

![]()

This chart shows some recent analysis calculations of various industry leaders. It may appear a bit self-promotional (and probably is), however it’s important as a benchmark item to help those in our profession understand how to critically appraise what costs we actually need to incur as part of doing business. For example, a $2,000,000 production practice would pay an extra $10,000 per year in transaction costs by adding 0.5% in transaction costs that come in addition to the interchange rates.

Even if you aren’t a client of OrthoFi (or will never be), it is important for everyone to know this information. It is our belief that a rising tide lifts all ships.

Here’s my advice:

1. Accept all cards: Since the opportunity cost of not accepting credit/credit cards far outweighs the cost for using them, eliminating credit card payments from your office or limiting which credit cards you accept isn’t logical. With consumers focused on racking up miles, points, rewards and even using certain credit cards as tax shelters, avoiding credit cards will often backfire on you and cost you valuable starts. With the average patient pool using AMEX only 5.2% of the time, even a few lost starts from arbitrarily blocking a particular payment method amounts to more than the incremental cost of just accepting them.

2. Rework your scripting: Just because you accept all payment methods doesn’t stop you from asking for an ACH routing number as your primary form of payment. “All we need to get started is a routing number or a cancelled check”. It’s a simple first step that would save you quite a bit in aggregate processing fees as ACH payments are under 1% compared with 2.0-3.5% typical with most credit cards. If they don’t want to pay from their checking account, ask next for a Visa or MasterCard. “No problem. How about a Visa or MasterCard?” Again, you want to start with the lowest typical fees and move up from there. You will still have people wanting to pay with AMEX or Discover, however you will decrease the overall mix of these cards, thereby lowering the total processing fees you pay.

3. Ask smarter questions: Be sure to understand all the costs (both advertised and otherwise) associated with payment processing. There are many companies out there competing for your business. The interchange fees are almost always what is used to lure people into switching payment processors. However, there are several other ways–typically not advertised or discussed–various providers will then use to increase your total net costs. Remember interchange fees are only one component of overall transaction costs. Before you take the bait, look for the hook. Be sure you understand all the transaction costs involved with your particular provider so you can make an informed decision about your credit card processor.

This article was originally published by Dr. Jamie Reynolds Novi, MI, USA

Dr. Jamie Reynolds earned his dental degree from the University of Michigan and his master’s degree in orthodontics from the University of Detroit-Mercy. He is a diplomate of the American Board of Orthodontics and the first orthodontist to include an Insignia case in his ABO re-certification examination. In private practice, he lectures nationally and internationally on the Damon System, advanced orthodontic technologies, soft-tissue lasers and aligners. His passion to make high-quality orthodontic treatment accessible to as many people as possible led him to co-found OrthoFi.